Taxation of the Rich, the Eumenes Paradox, and the Origins of Representative Government

Although merchants dominate later accounts, the most socially and ecoÂnomically relevant group in the medieval period, as sociologists Hechter and Brustein have also argued, was the nobility.[697] Noble compellence is critical in explaining the more extended territorial reach of the English Parliament, as we have seen.

In fiscal matters as well, when the most powerful were bound to the crown, whether by debt or taxation, the population under noble lordship was better integrated into the polityÂwide royal institutions; this was a real “trickle-down” effect.The idea that the English crown had strong extractive capacity, espeÂcially over the most powerful, however, counters assumptions not only of social scientists, but of some specialists as well. Historical sources strikÂingly depict “English kings [who] strained every nerve but could never be rich enough.”[698] But this is not surprising: the English were competing with France, which had three times the population.[699] Rather, surprising was that they managed to match, even exceed, the French in per capita extraction, as shown in the final section.

Nonetheless, English rulers are also claimed to have been highly constrained in their capacity to tax magnates especially when Parliament consolidated, in the 1290s.[700] A classic study of English taxation, by James Willard, asserts that the “people who were not wealthy paid the taxes of England in the thirteenth and fourteenth centuries just as they do today.”[701] This ties in well with common conceptions of the English crown as originally weak in extractive capacity.[702] Further, some historians point out that the tax burden of specific nobles was paltry. The Earl of Cornwall, who was probably the richest lay magnate in the 1290s and Edward I’s cousin, had “an annual income amounting to several thousand pounds.” Yet, his tax burden was trivial: in 1296, “he contributed about £10 to a tax on movables.” Another highly ranked but undertaxed noble was Roger, Earl of Norfolk.

His assessed direct taxes amounted to only 4.5 percent of his income on some of his properties between 1294 and 1298.[703] Such evidence appears dispositive - until it is contrasted with the loans and debts of some of these powerful actors to the crown, as done next.I then discuss the aggregate picture and further consider the mechanÂisms that link these observations.

6.1.1 Low Fiscal Burden for Nobles?

The Earl of Cornwall may have contributed only £10 in 1296, but he had lent the crown about £18,000, about 35 percent of the average annual tax raised by Edward I. Moreover, he was obliged to participate in battle and contribute troops. Further, he “was regularly summoned to parliament throughout the 1290s, served as a frequent witness to the king’s charters, and continued to advance major loans to the king and his courtiers.” When he died childless, his estate escheated to the crown. This most powerful magnate, therefore, was lightly taxed but delivered huge amounts to the crown without reimbursement.15

The Earl of Norfolk may have faced a similarly low rate on some of his income, but this amount also has to be set against extensive military service and financial debts, typically from commuted military obligations, to the crown. Roger participated in all the major Welsh and Scottish campaigns. Moreover, his incentives to be present and support Parliament were high: when he needed to negotiate his overdue debts that exceeded £2,000, he had to submit a petition in Parliament. He was also involved in royal adjudication, for instance “he was one of the magnates asked in 1292 to examine the pleadings” over who should succeed to the Scottish throne. Foremost, when he died, the crown took over his lands and office, “as had been agreed” when he was still alive.[704]

Drawing conclusions from tax obligations of a few highly placed nobles alone can therefore be misleading about the power relations involved.

Though a systematic picture is lacking, other earls might even be paying up to 50 percent of their community’s direct tax burden in the fourteenth century, as Ormrod has noted.[705] Next, I consider some aggregate eviÂdence about the burdens on the nobility flowing from their tenurial position and the high capacity of the crown.6.1.2 Low Fiscal Burden for Nobles? The Aggregate Evidence

Patterns of noble obligations to the crown can be reconstructed from prosopographic evidence in the Oxford Dictionary of National Biography introduced in Chapter 3, for the period from 1200 to 1350. As noted already, these data should not be confused with historical estimates; they simply offer a minimum that confirms what historians know but remains unquantified, namely that obligations did not exist just on paper but were enforced.

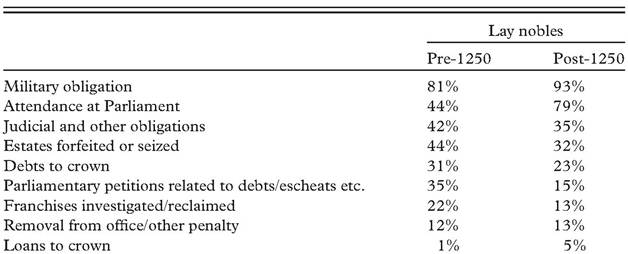

Before purely fiscal obligations are considered, a broader context of compellence must be noted that included military duties, penalties for not complying with duties, and of course the judicial obligations and parliamentary attendance discussed in Chapter 3, all of which had a fiscal dimension (Table 6.1). These obligations were almost universally enforced among the nobility - more than 93 percent are reported as serving militarily after 1250 in the ODNB,[706] whilst the lower number before that date (81 percent) draws on more limited records. Military obligation was tied to parliamentary summons: “the lists used for military summonses were used to identify those who should come to

Table 6.1 Financial ties between crown and lay nobility

Source: Oxford Dictionary of National Biography.

parliament”;19 both were mostly tied to land tenure. Those mentioned to have attended after 1250 reach almost 80 percent; they appear lower for the previous period, 44 percent, when records were scarcer, the crown weaker, and the institution less established.

More than a third of nobles are mentioned as having performed high judicial service, as a justice or hearer of petitions, reflecting the dynamics examined in Chapter 3. When obligaÂtions were violated, the crown imposed penalties, for instance removal from office. At least 12-13 percent in the two periods met that fate.The fiscal dependence of the nobility on the crown, on the other hand, is indicated primarily by five main measures: the seizure of estates by the crown as punishment for non-performance of obligations or wrongdoing, debts owed to the crown, parliamentary petitions for reduction of debt or other obligations, franchises (sets of privileges and exemptions) investiÂgated or reclaimed by the crown, and loans to the crown.

Only about 5 percent of nobles are mentioned as having lent funds to the crown after 1250, again probably an underestimate.20 However, nine out of thirteen lenders came from the top ranks, the earls. The small numbers were counterbalanced, therefore, by the disproportionate amounts involved - earls were, after all, the richest subjects. The social status of lenders also endowed these loans with disproportionate signifiÂcance, as we will see in the next section. That the nobility lent to default- prone, unconstrained sovereigns defies the concerns about expropriation in the neo-institutionalist literature.21 As Drelichman and Voth

19 Prestwich 2005, 131.

20 Historians have focused more on loans from external sources, for instance Italian bankers and merchants; Fryde 1955.

21 North and Weingast 1989.

provocatively showed for the 1500s, even “lending to the borrower from hell,” Philip II, could be profitable.[707] And nobles did not always lend to the crown for profit. Instead, obligation flowed from their tenurial status, creating an asymmetric exchange.

This asymmetric dynamic also underlies debt, which burdened “virtuÂally all the magnates” especially under Edward I, but which also remains unquantified.[708] Thirty-one percent of nobles are recorded as being debtÂors before 1250 and 23 percent after, though these are again surely underestimates.

The nobility mainly owed to the crown in the thirteenth century, with the crown owing more after the fourteenth.[709] Much debt originated in commuted military service (scutage), but also in various breaches. Clergy often paid in fines what they would have paid in taxes.[710] Or the king could pardon debts in exchange for military or other kind of service.[711] Edward I forced magnates to fight in Gascony by threatening to collect debts.[712] The exchange was not always quid pro quo bargaining; it was often done ex-post, as a reward.[713] Parliament in fact became an important locus for the submission of petitions related to debt, with at least 35 to 15 percent of nobles recorded as doing so in the two periods.Finally, a major indicator of royal power over the nobility was the crown’s capacity to either permanently “forfeit” or temporarily “seize” the land of royal tenants, if a breach had occurred. Greater security of property rights is widely assumed in England compared to Continental kingdoms, so it is striking to note that over 44 percent of nobles are mentioned as having their estates seized or forfeited before 1250, dropÂping to about 32 percent after that. These measures all attest the remarkÂable infrastructural capacity I have argued preceded and enabled the emergence of Parliament.

6.1.3 Political Effects of Fiscal Dependence? The Micro-Evidence

Fiscal dependence of the nobility on the crown shaped attitudes towards taxation in different ways. On the one hand, powerful lords habitually resisted royal penetration and extraction from their own tenants. For instance, earls’ bailiffs could prevent royal tax collectors from entering the counties, as did Edmund of Almain in 1290 or the Earl of Lancaster in 1319.[714] However, noble “inability to claim exemption” from taxation[715] also meant they had incentives to spread the burden.

The remarkable extractive powers of the English crown would not have materialized if resistance was greater than compliance.For instance, nobles who lent extensively to the crown might be incenÂtivized to be more open to royal authority penetrating the localities and taxing tenants across the polity separately, as taxation was needed to repay royal debt. Though few nobles lent so extensively early on, their preeminence in society meant that their preferences had wide societal effects. Support for representative practice of course was not a crude function of pecuniary goals of the uppermost nobility. Lending to the king was shaped by their prior relationship, which already aligned some of their interests (many were royal relatives). Nonetheless, it likely affected their stakes in this matter.

This hypothesis in fact explains at least some noble support for taxation other approaches leave unexplained or dismiss as a “representative pose.”[716] For instance, Maddicott mentions that Richard of Cornwall, the king’s brother, pressured knights and the clergy to accept a tax in the 1250s.[717] But Richard was also the “richest earl in England, and one of the richest men in Europe, [who] spent a large part of his fortune in supportÂing the regime of his feckless elder brother, Henry III.” Before 1254, he had made “massive loans” to the king.[718] He was also closely involved with the king’s military pursuits, and was given the mint to administer, which was a source of profit. Earls could also use their social prestige within their communities to legitimize taxation. When papal legates were raising a tax for the 1241 Crusade to the Holy Land, they invoked Earl Richard’s sanction. Owing to “the favour in which [he] was held,” Matthew Paris wryly observed, by “this method of draining the purses of the English, an immense sum of money was obtained.”34

Another major lender to the crown was the leader of the baronial revolt in 1258, Simon de Montfort, the king’s brother-in-law. The crown owed so much to him that the committee of twenty-four memÂbers who were entrusted with the government under the Provisions of Oxford also dealt with his debt.35 Since the Parliaments of 1264 and 1265, which Simon called, knights from the counties were somewhat more systematically summoned to serve as representatives, thus ensurÂing broader participation and engagement with the tax burden. Although we see such participation as an eagerly sought-after right, in practice it ensured that lower social orders were now actively involved in covering the king’s obligations, as explained in Chapter 4. This is not to be taken as a motive, but as an enabling condition that altered typical conflicts of interest in such circumstances. Further, the nobility coÂopted their own tenants by extending to them privileges from the crown as well.[719] Similar preferences might operate on debtors to the crown, on the margin: they might welcome taxation as reducing somewhat royal pressure to collect noble debts that were often handled through Parliament.[720]

Fiscal pressures on earls were not always in the same direction: excesÂsive taxation affected their own incomes, which reverts to the traditional fiscal logic, of demanding limits on taxation when faced with high extracÂtion. For instance, in 1297 the earls of Warwick and Arundel protested they were unable to contribute to the expedition in Flanders.[721] Earls could also defend others facing exorbitant royal demands, including the Church, as did the Earl of Cornwall.[722] And indebtedness was not deterÂministic: the Earl of Norfolk had large debts to the crown, but this led him to oppose the king in 1297.[723] However, although systematic evidence about all nobles who lent or owed to the crown and about their preferÂences on taxation is lacking, overlapping incentives towards the extension of representation can be discerned in some of the key actors in the formative thirteenth century.

If the nobility faced a fiscal burden, was the English system one that taxed the rich and spared the poor in the early stages of institutional formation? As late as 1327, the very poor were indeed exempt from taxation.[724] The poor were little taxed, though they generated much wealth that was taxed.[725] Unlike elsewhere in Europe, however, everyone else was taxed: from “the highest and the lowest of medieval fold, no one was free from the payment of taxes unless he had been granted the privilege of exemption,” and these were few in the early 1300s.43 Individual assessments were replaced by quotas in 1334, however;[726] by the 1370s, assessments were frozen at the levels of 1334, and taxation became regresÂsive, though the crown strove to counteract this trend, as Ormrod has noted in a nuanced assessment.[727] It is no accident that English constituÂtional history became more turbulent as the tax burden shifted. Nonetheless, Parliament as an institution was sufficiently entrenched so as to serve as the locus for most subsequent conflict and change.

The next section examines the striking contrast with France in the period of institutional emergence.

6.2